Posts Tagged ‘Accounting’

Normal Balance: Asset

The normal balance of an Asset Account is a Debit. So, if you had $1,000 in a bank account, it means you have a $1,000 Debit in the bank account.

Read More

How to Make QuickBooks® More User-Friendly Book

Just thought I’d share a little info about my book, How to Make QuickBooks® More User-Friendly: Simple changes to streamline your workflow in QuickBooks® Desktop. It’s available in eBook, Paperback, and Kindle format. See the description and video about the book below. Streamline your workflow in QuickBooks® with some simple, one-time changes. Follow along as…

Read More

Three Tips to Help You Mind Your Business

Three Tips to Help You Mind Your Business As a small business owner, you need to have a pulse on #allthethings, meaning Human Resources, Marketing, Product/Service Development, and so many other topics… including Accounting. This post will help you Mind Your Business with my three best tips I see people like yourself struggling with every…

Read More

Debits = Credits

Debits must always equal Credits. On every transaction the total of the Debits must equal the total of the Credits. In some transactions you may have more than one Debit and only one Credit. Or you may have one Debit and more than one Credit. Regardless the total value of Debits must equal the total…

Read More

What’s a Journal Entry?

The Journal Entry is used to record a transaction. It must include at least one Debit and least one Credit. The Debits and the Credits in the Journal Entry must equal. Journal Entries are used all throughout accounting.

Read More

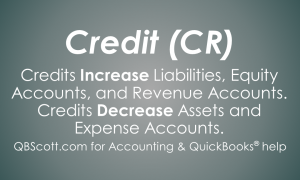

Credits (CR)

Credits are the opposite of Debits. Credit increase Liabilities, Equity Accounts, and Revenue Accounts. They also decrease Assets and Expense Accounts.

Read More

Debits (DR)

Learning about Debits (abbreviated DR) and Credits (abbreviated CR) can be confusing. However, if you keep in mind that Debits increase Asset and Expense accounts and decrease Liabilities, Equity Accounts, and Revenue Accounts, you’ll be half way there to understanding Debits and Credits.

Read MoreHow to Make QuickBooks® More User-Friendly eBook – Available Now!

Just thought I’d post a quick message about my new eBook: How to Make QuickBooks® More User-Friendly, Simple changes to streamline your workflow in QuickBooks® Desktop. This eBook was derived from my video training course with the same title. It is approximately 50 pages with nearly 60 screen captures with step-by-step instructions. I cover the…

Read More

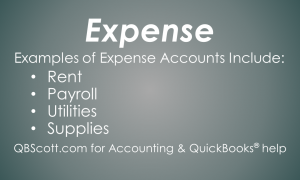

Examples of Expenses

Expenses are what a company has incurred or used up and are shown on a Profit and Loss Report. Expenses can include Rent, Payroll, Utilities, and Supplies.

Read More

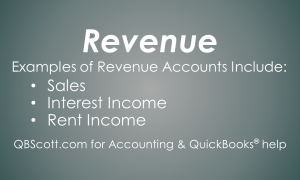

Examples of Revenue

Revenue is what a company has earned and is shown on a Profit and Loss Report. Revenue can include Sales, Interest Income, and Rent Income.

Read More